Bankruptcy Hell - The Sequel to ForeclosureGate

A major study of bankruptcy courts across the United States revealed that 50% of bankruptcy rulings were made without the required documentation from creditors. Ignore the law and make it easy for the big banks and others creditors - justice in the United States

You're headed for bankruptcy court tomorrow. It's been a long and difficult road. You and your husband both worked. You made decent money. Then your husband became ill. There was no sick leave because he worked for himself. His disability insurance had a six-month delay and only covered half of the lost income. That was all you could afford. (Image Wikimedia Commons)

His condition was critical and required medication three times a day at a monthly cost of $2500. Your company plan covered your husband but it didn't cover the medication because the insurance company termed it experimental. It was the sole option for the crippling illness according to the three specialists consulted.

Your husband contributed 40% of the family income. The loss was a big hit but you persevered. You couldn't sell the house, even if you wanted to. It was $150,000 upside down. There was no federal or bank program to relieve that burden. After four months of cashing in a modest 401(k), it became obvious that you couldn't make it. You needed relief and time for your husband to get well.

You consulted your accountant. On his advice, you decided to file for bankruptcy.

![]()

It was hard to find an attorney to take your case. The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 made attorneys personally liable for any false claims by filers. That created a lot of extra work and a new risk for bankruptcy attorneys to serve a population that was, by definition, short of cash for legal fees.

When you did get an attorney, you found out that the new bankruptcy law of 2005 requires credit counseling within six months prior to filing (a provision of little value to you)

By the time you got your day in court, you were well overdue for debt relief.

Here is what happened in bankruptcy court for the Chapter 13 filing.

The Bank Challenges Your Claim Alleging Fraud

The new bankruptcy law changes things for debtors. In the past, only "substantial abuse" by debtors led to an automatic dismissal of the case. The new law replaced a "a substantial abuse" with "an abuse" Section 102. In the past, only the U.S. Bankruptcy Trustee, an officer of the court, could charge fraud. Creditors now have that option (many of whom stand accused of fraud themselves).

When you got to court, you find out that your bank, MegaCorp, filed a charge of fraud claiming an understatement of your credit card debt. These charges are wrong but you lose a lot of sleep worrying about a violation that has a $250,000 fine and a nine-year prison term.

Before the favorable ruling from the court, you look at the U.S. Trustee Program web site for bankruptcy court.

It is obvious that the Department of Justice program is only interested in debtor fraud. There is no solicitation by the program for creditor fraud reports. Just debtors.

"Name and address of the person or business you are reporting.

"Identify the type of asset that was concealed and its estimated dollar value, or the amount of any unreported income, undervalued asset, or other omitted asset or claim." US Trustee Program

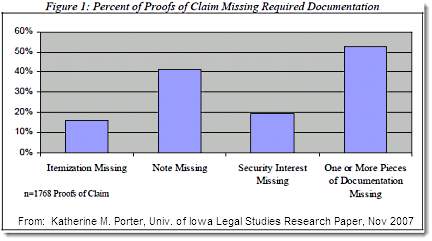

The Bank Leaves out Documentation Critical to Lawful Approval of their Claims against You

Kathleen M. Porter published a landmark study on bankruptcy court in 2007. Porter's research team reviewed 1700 bankruptcy rulings from federal courts across the country. Porter found that required documentation was missing in just over 50% of the cases from the extensive sample.

From, Misbehavior and Mistake in Bankruptcy Mortgage Claims, Katherine M. Porter, November 2007 p. 18

Professor Porter commented on this failure to comply with documentation requirements:

"Without documentation of the debt, the debtor and other creditors cannot verify the legitimacy or accuracy of claims, each of which cuts into the limited dollars available for distribution. Poor compliance with the claims rules effectively deflects creditors’ obligations onto cash-strapped bankrupt families, who must choose between the costs of filing an objection or the risks of overpayment." K.M. Porter, 2007 p. 36

Porter's research confirmed that only a minority of bankruptcy courts use incomplete documentation to disallow creditor claims. The failure to require proper documentation distorts over 50% of settlements. How can a bankruptcy judge set amounts owed, etc. without knowing the basis for such judgments?

The creditors with the special right to accuse you of fraud get away with filing flawed claims against you. Are their cases dismissed for errors? Hardly ever, according to the study.

You had no idea that the creditor clams were incomplete thus legally flawed. Neither the court nor your lawyer noticed.

There are Creditor Fees that You Don't Understand

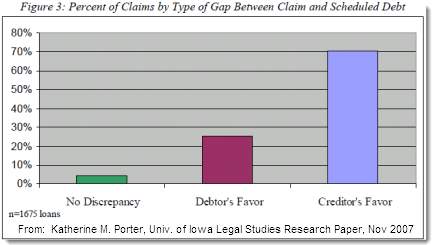

The paper chase of bankruptcy often times produces conflicting claims about amounts due. Debtors face tremendous pressure to readjust their entire lives to cope with impending financial doom. The graph below shows that creditors are much more likely to state claims in their favor than are debtors.

From, Misbehavior and Mistake in Bankruptcy Mortgage Claims, Katherine M. Porter, November 2007 p. 30

Debtors often listed more than they owed. Creditor usually listed more than they were due. Porter's extensive analysis suggested the following:

"Creditors' claims may themselves be bloated and overstate the accurate amount of the debt. Such problems could result from servicers’ practices of loading claims with default fees that are not disclosed to debtors, or because of mistaken calculations of the amount due in preparing the proof of claim; case law has documented both effects." K.M. Porter, 2007 p. 34

Once again, the debtors take the hit, the very people lacking the resources to challenge what they strongly suspect are creditor overstatements of debt.

You knew something was wrong but you didn't have the time or money to challenge your creditor's figures.

The Bank Claim is Approved

You suspect errors in the creditor claims but you can't prove that their figures are overstated. You do not know that your creditors are missing documentation, an error that should nullify their claims.

When debtors make a mistake, their case is subject to dismissal and they face severe penalties. When the courts receive and approve flawed, unlawful creditor filings in 50% of the cases, the court isn't even conducting a cursory review of essential documents. With any degree of diligence, most or all of the flawed creditor filings would be dismissed.

This proves, beyond any doubt, that in many cases, bankruptcy proceedings move forward without creditor adherence to clearly stated legal requirements.

The sole purpose of the court is to enforce the law. That simply doesn't happen for at least 50% of the cases judged.

Later, You Find Out that the Critical Documents were Missing and the Charges were Bogus

How could the bank prevail in this matter, you ask. The bank made a claim that they knew or should have known was false. The bank failed to present documents required from creditors, documents essential to judging the claim and making it conform with the law. The bank also included charges that were wrong and fees that were not warranted. Will the bank be charged with fraud? You want to challenge the ruling in favor of the bank but you're out of money. You now understand why most bankruptcy not contested

Bankruptcy Hell - Abandon hope all ye who enter here

There is no justice guaranteed for the weak, disadvantaged, poor, or dispossessed. Debtors filing bankruptcy operate on a limited budget and simply want the nightmare to end. They want to get on with their lives. They often lack the ability to make legal challenges. When their lawyers don't inform them of those challenges, they have no options.

In the 50% of the cases where critical documents were missing, their lawyers fail to make the challenge. Worse still, in those and other cases where creditor filings are obviously deficient and outside the law, the court misses the error.

Wouldn't it be better if bankruptcy court operated like, let's say, an automobile manufacturer. Honda issued a recall on airbags for 2001 and 2002 models.

"Honda has expanded a previously announced recall of certain 2001 and 2002 model-year vehicles to replace the driver's airbag inflator in an additional 378,758 vehicles in the U.S. … In total, Honda is aware of 12 incidents related to this issue as of February 2010." Honda February 9, 2010

Based on 12 incidents brought to their attention, Honda recalled every vehicle suspected, nearly 400,000.

At least seven federal courts have cited Katherine Porter's study Her study included over 1,700 cases., half of which had a defective part - missing documentation required by law to justify the bankruptcy. Compare 850 instances of a defective part with no corrective action to the twelve instances referenced by Honda that generated a universal recall of models for two consecutive years.

Perhaps, the federal bankruptcy courts should emulate the judgment and practices of Honda.

The failure of bankruptcy courts to apply the law equally and the refusal to go back and correct every error in judgment demonstrate that we are clearly not a nation of laws. We are a nation in which the front room of the law serves the back room of The Money Party.

END

This article may be reproduced entirely or in part with attribution of authorship and a link to this article.

del.icio.us |

del.icio.us |

Digg

Digg

Post your comment